The Ultimate Guide to Global E-Commerce Tax and Compliance in 2026: Essential Business Rules for Cross-Border Sellers

Entering 2026, global e-commerce is no longer just a competition of traffic, product selection, and logistics. For cross-border sellers, Shopify independent stores, marketplace sellers, DTC brands, dropshipping sellers, and one-piece fulfillment service providers, tax and compliance are becoming key factors that determine whether a store can operate sustainably in the long term.

In the past, many sellers were used to selling products first and then gradually fixing tax issues, documents, and compliance materials later. But the market environment in 2026 has changed significantly. Tax authorities, customs agencies, platforms, payment companies, and consumer protection regulators around the world are forming a more connected data supervision system. Once sellers ignore tax and product compliance, they may face parcel detention, product delisting, account suspension, tax recovery, customer complaints, and even damage to brand reputation.

This is especially important for cross-border small parcels, low-ticket products, overseas warehouse fulfillment, multi-channel marketplace sales, and direct-to-consumer independent store models. These business models now require more upfront planning than before. The United States has already suspended duty-free de minimis treatment for low-value goods from all countries. The previous logic that packages valued at $800 or below could enjoy low-value duty-free treatment has changed significantly. According to U.S. CBP, imported goods valued at $800 or below from all countries are no longer eligible for de minimis duty-free treatment and must be subject to applicable duties, taxes, fees, and customs clearance requirements.

The European Union is also strengthening supervision of low-value small parcels. The Council of the European Union confirmed that from July 1, 2026, small parcels entering the EU with a value below €150 will be subject to a temporary fixed customs duty of €3 per product category. This temporary arrangement is planned to last until July 1, 2028.

This means that cross-border e-commerce sellers in 2026 can no longer focus only on product cost, shipping cost, and advertising cost. You must also understand who bears the taxes, how customs duties are calculated, whether VAT/GST registration is required, whether the platform collects and remits tax on your behalf, whether the product meets safety standards, whether customer data is handled compliantly, and whether invoices and order records are complete.

This article will systematically explain the core logic of global e-commerce tax and compliance in 2026, covering major global markets, common tax types, the United States, the European Union, the United Kingdom, Australia, Canada, Singapore, Japan, and practical operating procedures for sellers.

1. Why E-Commerce Sellers Must Pay Attention to Tax and Compliance in 2026

Before 2026, many small and medium-sized sellers focused mainly on finding winning products, running ads, testing creatives, and improving conversion rates. These remain important, but they are no longer enough.

Today’s cross-border e-commerce environment is undergoing three obvious changes.

First, low-value parcel supervision is becoming stricter. Both the United States and the European Union are strengthening tax and customs management for cross-border e-commerce small parcels. In the past, some sellers relied on low-cost direct shipping, low declared values, duty-free parcels, and unclear customs clearance practices to gain price advantages. But this room for flexibility is shrinking.

Second, platform responsibilities are becoming heavier. Platforms such as Amazon, eBay, Etsy, TikTok Shop, Temu, and Walmart Marketplace are increasingly required in more countries and regions to handle tax collection, seller identity verification, transaction data reporting, and product safety governance. The EU DAC7 requires platform operators to report identity and financial information of relevant EU sellers to tax authorities each year, including seller personal or business information and revenue earned through the platform.

Third, product compliance and tax compliance are becoming connected. Sellers not only need to know how to collect and report tax, but also need to prove that their products are safe, properly labeled, supported by compliant instructions, and backed by clear responsible party information. The EU General Product Safety Regulation, or GPSR, has applied since December 13, 2024, replacing the previous General Product Safety Directive and aiming to strengthen consumer product safety protection.

Therefore, cross-border e-commerce compliance in 2026 is no longer a single financial issue. It is a complete system that runs through product selection, procurement, listing, pricing, logistics, payments, after-sales service, and brand operations.

2. The Most Common Tax Types Global E-Commerce Sellers Encounter

The tax issues commonly faced by cross-border e-commerce sellers are mainly concentrated in the following categories.

1. VAT / GST / Consumption Tax

VAT, GST, and consumption tax are essentially indirect taxes applied at the consumption stage. They are usually borne by consumers, but sellers or platforms are responsible for collecting them at the time of sale and filing and paying them according to regulations.

Common examples include:

EU VAT, UK VAT, Australian GST, Canadian GST/HST, Singapore GST, Japanese Consumption Tax, and others.

For cross-border sellers, VAT/GST most commonly appears in the following situations:

Sellers sell goods to local consumers;

Sellers store inventory in a local overseas warehouse;

Sellers sell through a platform and the platform collects part of the tax;

Sellers sell directly to consumers through an independent store;

Sellers sell digital products, subscription services, or remote services.

Many beginners mistakenly believe that “my company is not located there, so I do not need to care about local tax.” This understanding is very risky in 2026. Many countries now determine tax obligations based on sales destination, customer location, platform responsibility, and inventory location.

2. Sales Tax

Sales Tax mainly applies in the United States. The United States does not have a unified national VAT system. Instead, sales tax is managed at the state and local levels.

For e-commerce sellers, the key is to determine whether nexus has been created in a particular state. Even if a seller does not have a U.S. company, office, or employees, if sales or transaction volume in a certain state reaches that state’s economic nexus threshold, the seller may need to register for a sales tax permit, collect sales tax from consumers, and file and remit tax. The 2026 state-by-state guide from Sales Tax Institute states that all states with sales tax have economic nexus requirements for remote sellers.

3. Import Duty / Customs Duty

Import duty is a tax that may be incurred when goods enter a target country or region. It is usually related to the product’s HS Code, country of origin, declared value, trade policy, and customs clearance method.

In 2026, sellers should pay special attention to low-value parcel changes in the United States and the European Union. In the past, some low-ticket products could enter markets through small parcel exemptions or lower customs clearance costs. This model is now being reassessed.

4. Income Tax / Corporate Tax

Income tax is a tax on company profits. It is usually related to the place of company registration, place of effective management, permanent establishment, employee location, warehouse location, and business substance.

For example, a Chinese company selling products to U.S. consumers through Shopify may involve U.S. sales tax, import duties, and Chinese corporate income tax. If the seller establishes a U.S. company or uses a U.S. local warehouse for a long time, more complex income tax and state tax issues may arise.

5. Platform Reporting

Platform reporting is not a new tax, but it makes seller income increasingly transparent. The United States has Form 1099-K, the European Union has DAC7, and many countries are also requiring platforms, payment institutions, and e-commerce operators to report seller income and identity information to tax authorities.

The IRS explains that if a seller receives payments for goods or services through payment apps or online marketplaces and exceeds $20,000 and more than 200 transactions, the payment platform generally needs to issue Form 1099-K. Platforms may also issue this form at lower amounts or transaction volumes.

This has a direct impact on e-commerce sellers: platform backend sales, payment platform deposits, bank statements, accounting reports, and tax filings must be reconcilable.

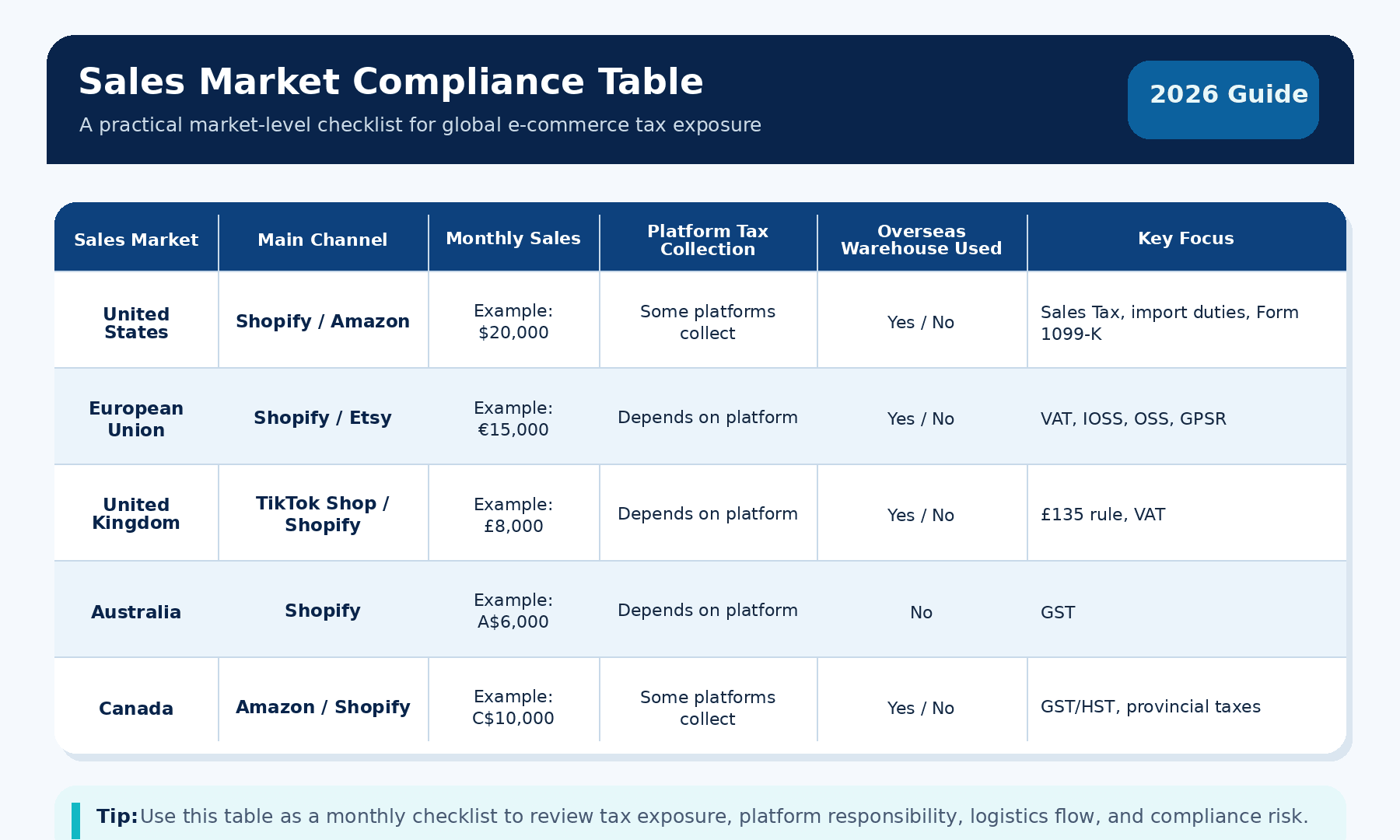

3. The U.S. Market: Sales Tax, Form 1099-K, and Import Rules Are the Core

The U.S. market has a large volume and strong consumer purchasing power, making it a key market for many cross-border sellers. However, the U.S. tax system is relatively complex, especially sales tax and import rules.

1. U.S. Sales Tax Must Be Judged State by State

U.S. Sales Tax is not a unified national rule. It is a state and local tax system. Sellers need to determine whether they have triggered economic nexus in a specific state.

Common triggering factors include:

Sales in a state reaching the threshold;

Transaction volume in a state reaching the threshold;

Inventory in a state;

Use of a U.S. overseas warehouse;

Use of FBA causing inventory to enter different states;

Employees, offices, agents, or offline activities in a state.

If a seller only sells through platforms such as Amazon, the platform may act as a marketplace facilitator in many states and collect and remit sales tax on behalf of the seller. But if the seller also operates a Shopify independent store, TikTok Shop external checkout, private-domain orders, or B2B wholesale, platform tax collection may not cover all sales channels.

2. Platform Tax Collection Does Not Mean Sellers Have No Responsibility

Many sellers mistakenly think: “Amazon already collects tax, so I do not need to worry about U.S. sales tax.” This is only partly correct.

If all your sales come from platforms, and the platform assumes marketplace facilitator responsibility in the relevant states, then the platform may collect and remit sales tax for that portion of sales. But you still need to keep order records, platform reports, refund records, and income records.

If you have independent store orders, or if certain channels are not covered by platform tax collection, you still need to determine whether registration and filing are required.

3. Form 1099-K Makes Seller Income More Transparent

Sellers receiving payments through PayPal, Stripe, platform payments, and third-party payment tools need to pay attention to Form 1099-K. Even if you do not receive Form 1099-K, it does not mean the income does not need to be reported. Form 1099-K is more of an information reporting tool used to help tax authorities understand transaction data on payment platforms.

Sellers should focus on managing the following data:

Platform sales;

Payment platform receipt amounts;

Refund amounts;

Transaction fees;

Advertising costs;

Logistics costs;

Procurement costs;

Bank deposit amounts;

Accounting profit.

If these data points remain messy for a long time, tax explanations later will become very difficult.

4. The U.S. Low-Value Parcel Exemption Logic Has Changed

In 2026, the most important thing to recalculate for the U.S. market is import cost. U.S. CBP clearly states that imported goods valued at $800 or below are no longer eligible for de minimis duty-free treatment.

This has a major impact on the following models:

Direct shipping from China to U.S. consumers;

Low-ticket small parcels;

One-piece dropshipping;

Logistics channels relying on low declared values;

Products with low prices, thin margins, and heavy weight;

Independent stores relying on “free shipping and tax included” to attract customers.

Sellers need to recalculate product prices, customs clearance costs, duties, logistics timelines, and return costs. They cannot continue using old profit models.

4. The EU Market: VAT, OSS, IOSS, DAC7, and GPSR Must Be Considered Together

The European Union is one of the most systematic and confusing compliance markets for cross-border e-commerce sellers.

1. EU VAT Is the Core

When EU consumers purchase goods, VAT is usually involved. VAT rates vary by country. Sellers need to determine tax treatment based on product type, sales method, shipping origin, and customer location.

If sellers conduct B2C distance sales within the EU, they can use OSS to simplify filing. According to EU official information, the previous country-by-country thresholds for intra-EU distance sales have been replaced by a unified €10,000 threshold, and online sellers can use OSS to report relevant VAT across the EU in one Member State.

2. IOSS Applies to Some Low-Value Imported Goods

IOSS mainly applies to low-value imported goods sold from outside the EU to EU consumers with a value not exceeding €150. Its purpose is to allow sellers to collect VAT at the time of sale and reduce extra tax payment and customs friction when consumers receive parcels.

But IOSS is not a universal solution. The following situations usually require separate assessment:

Goods valued above €150;

Use of EU overseas warehouses;

B2B orders;

Special products;

Platforms being treated as deemed suppliers;

Sellers not using IOSS numbers correctly;

Logistics providers or customs brokers not declaring correctly.

3. Changes to Customs Duties on Goods Below €150 Will Affect Low-Price Products

The EU previously offered a significant customs duty advantage for goods below €150, but this begins to change in 2026. According to information from the Council of the European Union, from July 1, 2026, each product category in small parcels entering the EU will be subject to a temporary fixed customs duty of €3. The temporary measure is planned to last until July 1, 2028.

This has a strong impact on low-ticket products. For example, for small products priced at €9.99, €14.99, or €19.99, once VAT, platform commissions, advertising costs, international shipping, fixed customs duties, and return costs are added, profit margins may shrink significantly.

4. DAC7 Makes Platform Sales More Transparent

DAC7 requires platform operators to report the identity and financial information of relevant EU sellers to tax authorities. Platforms need to conduct due diligence and report sellers’ revenue data.

For sellers, this means platform revenue is no longer just internal platform data. Sellers should ensure that platform backend data, payment platforms, bank statements, and tax filings have a clear correspondence.

5. GPSR Strengthens Product Safety Responsibilities

The EU GPSR applies to a wide range of consumer products and especially affects cross-border e-commerce, online platforms, and brands selling directly to EU consumers. It requires products entering the EU market to have more complete safety information, traceability, and responsible parties. GPSR has applied since December 13, 2024.

If you sell toys, children’s products, electronic products, battery-powered products, personal care products, kitchenware, pet products, outdoor products, or products that contact the skin, you must not ignore GPSR.

Sellers need to prepare in advance:

Product safety instructions;

Product labels;

Manufacturer information;

EU responsible person information;

Batch numbers or product identification information;

Test reports;

Warning statements;

Recall procedures;

Customer complaint handling records.

5. The UK Market: The £135 Rule and VAT Registration Require Close Attention

After Brexit, the United Kingdom has its own VAT system. For cross-border e-commerce sellers, the most important point is the £135 rule.

HMRC explains that if goods valued at no more than £135 are located outside the UK at the time of sale and are sold to UK consumers through an online marketplace, UK VAT is usually handled at the point of sale. If goods are sold directly to UK consumers through non-platform channels, corresponding point-of-sale VAT rules also apply.

Sellers need to pay special attention to the following situations:

Goods shipped directly from China to UK consumers;

Sales to UK customers through a Shopify independent store;

Use of a UK overseas warehouse;

Sales through platforms such as Amazon UK or eBay UK;

Goods valued above £135;

Whether the customer is an individual or a business;

Whether the seller acts as the importer;

Whether UK VAT registration is required.

If a seller uses a UK overseas warehouse, it usually creates a stronger UK VAT obligation than direct shipping from China. Once inventory is stored locally in the UK, local tax registration and filing responsibilities may be triggered.

6. Key Points for Australia, Canada, Singapore, Japan, and Other Markets

1. Australia: GST on Low-Value Imported Goods

The standard GST rate in Australia is 10%. The ATO explains that GST may apply when non-resident businesses sell goods with a customs value of A$1,000 or less to Australia. The ATO also states that the Australian GST rate is 10%.

If your independent store sells to Australian consumers for a long time, you need to pay attention to whether you have reached the GST registration threshold, whether the platform collects tax, whether product prices include tax, whether invoices are compliant, and how GST is handled when refunds occur.

2. Canada: GST/HST and Provincial Taxes Should Not Be Confused

Canada has a federal GST/HST system, while some provinces also have PST, QST, and other provincial taxes. The Canada Revenue Agency explains that GST/HST measures related to the digital economy have taken effect, and registered businesses generally need to collect GST/HST from consumers and remit it to the CRA.

For cross-border sellers, the difficulty of the Canadian market is that it is not just about one national tax rate. Different provinces, different products, and different sales methods may affect tax treatment.

3. Singapore: GST Registration Threshold for Overseas Vendors

Singapore’s IRAS explains that if an overseas business has annual global turnover exceeding S$1 million and makes more than S$100,000 of B2C remote services and/or low-value goods supplies to Singapore customers, it must register for GST. After registration, it must collect and account for GST on the relevant B2C supplies.

This is especially important for sellers of digital products, subscription services, online courses, SaaS services, or low-value goods to Singapore.

4. Japan: Consumption Tax and Platform Responsibilities Continue to Strengthen

The Japanese market has high expectations for quality, packaging, instructions, and after-sales service. When selling physical goods, sellers need to pay attention to import consumption tax, customs clearance, product labels, Japanese-language instructions, platform sales rules, and after-sales responsibilities.

If you sell digital services or operate a platform-type business, you also need to pay attention to Japan’s requirements for platform responsibility and consumption tax filing. For sellers of physical goods, Japan is not only about taxes and fees, but also about product localization and customer experience.

7. Beyond Tax: These Compliance Areas Also Matter in 2026

1. Product Safety Compliance

Product safety compliance is one of the most easily overlooked risks in cross-border e-commerce. Many sellers only care whether the supplier can ship, whether the price is low, and whether the product images look good, but they do not confirm whether the product can be legally sold in the target market.

High-risk categories include:

Children’s toys;

Baby and toddler products;

Electronic and electrical products;

Wireless devices;

Battery-powered products;

Beauty and personal care products;

Food contact materials;

Kitchenware;

Pet products;

Sports and outdoor products;

Medical and health-related products.

Sellers should request test reports, material descriptions, product labels, instructions, warning statements, production batch information, and compliance certificates from suppliers. Do not simply accept the supplier’s statement that “we have certificates.” The certificate must correspond to the specific product, model, material, manufacturer, and target market.

2. Platform Identity Verification

Platforms will become increasingly strict in verifying seller identities. The EU Digital Services Act imposes higher requirements on online services and platforms, covering online marketplaces, social networks, app stores, and other digital services.

Sellers need to ensure consistency among the following information:

Business license;

Company address;

Legal representative or beneficial owner information;

Bank account;

Tax number;

VAT/GST registration information;

Warehouse address;

Return address;

Brand authorization documents;

Product responsibility documents.

If these documents contradict one another, platform review may easily trigger risk controls.

3. Privacy Policy, Cookies, and Advertising Tracking

Independent store sellers should not only focus on ad conversion but also on user data compliance. EU official information explains that certain cookies require user consent before collecting user data and cannot be set automatically when a webpage opens.

If your website targets EU customers, it is recommended to prepare at least:

Privacy Policy;

Cookie Policy;

Cookie consent banner;

User data deletion request channel;

Email marketing consent mechanism;

SMS marketing consent mechanism;

Data processing explanation;

Third-party advertising tool disclosure.

If you target California consumers in the United States, you should also pay attention to the CCPA. The California Department of Justice explains that the CCPA applies to for-profit businesses operating in California that meet certain thresholds, such as annual revenue exceeding $25 million, buying, selling, or sharing personal information of 100,000 or more California residents or households, or deriving 50% or more of annual revenue from selling California residents’ personal information.

8. Practical Compliance Workflow for Cross-Border E-Commerce Sellers in 2026

For cross-border e-commerce sellers, tax and compliance should not be fixed only after the store starts generating orders. The correct approach is to embed compliance into the entire operating system before product selection, pricing, store building, listing, shipping, and after-sales service.

This workflow is suitable for Shopify independent stores, Amazon/eBay/Etsy marketplace sellers, TikTok Shop sellers, dropshipping sellers, one-piece fulfillment sellers, overseas warehouse sellers, and DTC brands.

Step 1: Confirm Your Sales Markets First

Sellers must first clearly identify which countries and regions they are selling to. Many beginners simply say,“I sell to Europe and the United States,” but Europe and the United States themselves contain many different tax systems.

The United States involves state sales tax, import duties, and Form 1099-K information reporting. The European Union involves VAT, OSS, IOSS, DAC7, GPSR, and responsible persons. The United Kingdom has its own VAT rules and the £135 rule. Australia has GST. Canada has GST/HST and may also involve provincial taxes. Singapore, Japan, and other markets also have their own consumption tax and import rules.

Therefore, sellers should first prepare a sales market table:

The purpose of this step is not to immediately register tax numbers in every country, but to first understand which markets already have potential tax obligations and which markets can continue to be monitored.

Step 2: Map Out Your Shipping Model

After confirming your sales markets, the second step is to check where the goods are shipped from. In cross-border e-commerce, tax risks are often not determined by the location of the store, but by the flow of goods, inventory location, and importer identity.

Common shipping models include:

Chinese suppliers shipping directly to overseas consumers;

Chinese dropshipping service providers handling procurement, quality inspection, packaging, and shipping;

Inventory stocked in U.S. overseas warehouses in advance;

Inventory stocked in UK or EU overseas warehouses in advance;

Use of Amazon FBA;

Use of third-party 3PL warehouses;

Suppliers shipping directly while the seller handles payment collection and after-sales service.

Different shipping models correspond to different tax responsibilities.

If you ship directly from China, you need to focus on import VAT, customs duties, IOSS, DDP/DAP, and customs declarations.

If you use EU or UK overseas warehouses, local VAT registration may be required.

If you use U.S. overseas warehouses, in addition to sales tax, inventory location may create stronger tax nexus.

If you sell through platform warehousing, the platform may collect some taxes, but this does not mean all responsibilities belong to the platform.

Sellers should clearly map the following chain for each major market:

**Where the product ships from → Who is the importer → Who handles customs clearance → Who bears taxes and duties → Whether the platform collects tax → Whether the seller needs to register a tax number → How after-sales returns are handled.**

Once this chain is clear, pricing, listing, and after-sales policies will not become confusing.

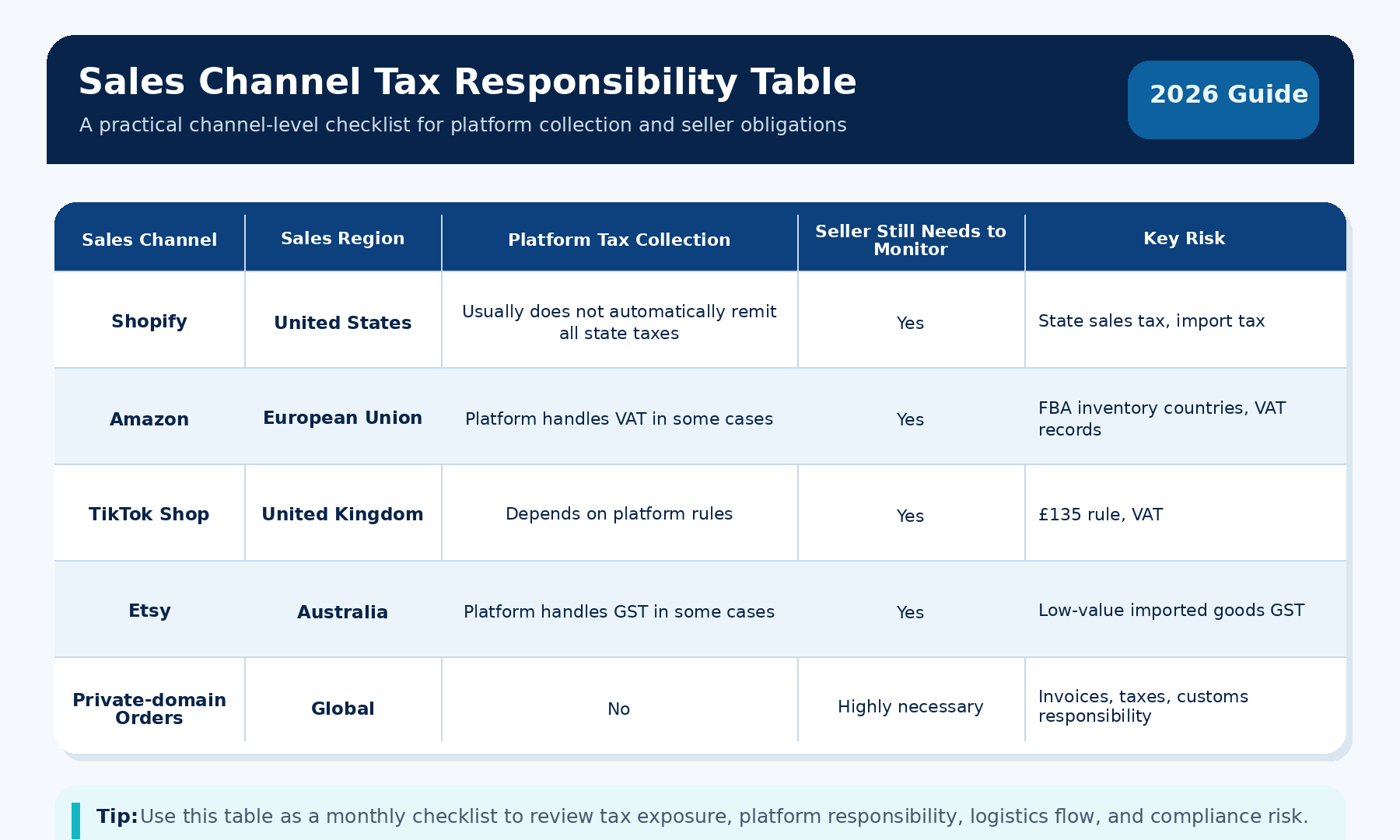

Step 3: Confirm the Tax Responsibility of Each Sales Channel

Cross-border sellers usually operate more than one sales channel. Many sellers run Shopify, Amazon, eBay, TikTok Shop, Etsy, Walmart Marketplace, and even WhatsApp private-domain orders and B2B wholesale orders at the same time.

At this point, sellers cannot mix all orders together. They need to break them down by channel.

For marketplace orders, first confirm whether the platform collects and remits VAT, GST, or Sales Tax. Many platforms collect tax on behalf of sellers in some countries and regions, but this rule does not necessarily cover all markets, all products, and all orders.

For Shopify independent store orders, sellers usually need to set tax rates, determine tax obligations, keep transaction records, and register and file once thresholds are met.

For private-domain or B2B orders, sellers also need to confirm buyer identity, invoice requirements, import responsibility, and whether reverse charge rules apply.

It is recommended to create a channel tax table:

The value of this table is that it prevents sellers from mistakenly thinking, “The platform already collected tax, so all channels are safe.”

Step 4: Recalculate Product Profit

In 2026, cross-border e-commerce profit cannot be judged only by “product cost + shipping cost + advertising cost.” Tax and compliance costs must be included in the product pricing model in advance.

A complete profit model should include at least:

Product procurement cost;

Domestic warehousing fees;

Quality inspection fees;

Packaging fees;

Brand customization fees;

International logistics fees;

Customs clearance fees;

Import duties;

VAT, GST, or Sales Tax;

Platform commissions;

Payment processing fees;

Customer acquisition advertising costs;

Refund costs;

Refusal costs;

Return costs;

Exchange rate losses;

After-sales reshipment costs;

Compliance testing or certificate costs.

This is especially important for low-ticket products, where tax and customs clearance costs have a very obvious impact on profit. For products priced at $9.99,€14.99, or £19.99, once platform commissions, advertising costs, VAT, customs duties, shipping costs, and return losses are added, the real profit may be much lower than expected.

Before listing each product, sellers should run three types of profit calculations:

**Ideal Profit**: Profit when there are no refunds, no tax anomalies, and logistics run smoothly.

**Normal Profit**: Profit after including average refund rate, advertising costs, platform fees, and taxes.

**Risk Profit**: Profit after including refusals, reshipments, customs duty increases, and logistics price increases.

Only when all three scenarios are acceptable should the product be considered suitable for long-term sales.

Step 5: Set the Correct Price and Tax/Fee Display Method

Many cross-border seller complaints do not come from the product itself, but from unclear tax and fee explanations. If customers think taxes are included when placing an order, but are asked to pay customs duties or VAT upon delivery, they are likely to refuse the parcel, leave negative reviews, or request refunds.

Therefore, independent stores and platform sales must clearly answer three questions:

Does the product price include tax?

Does the shipping fee include customs clearance costs?

Are import taxes and duties borne by the seller or the buyer?

If you use DDP, meaning the seller bears import taxes, duties, and customs clearance responsibility, the page can clearly state:

Taxes and duties included.

No extra customs fees on delivery.

Import duties are prepaid by the seller.

But the prerequisite is that you have truly calculated these taxes and fees into your costs.

If you use DAP, meaning the buyer may need to pay taxes and fees at import, then the product page, checkout page, Shipping Policy, FAQ, and order emails should all explain this in advance to avoid customers only discovering the extra tax upon delivery.

For Shopify independent store sellers, it is recommended to display the tax and duties policy in the following places:

Product page;

Cart page;

Checkout page;

Shipping Policy;

FAQ page;

Order confirmation email;

Logistics tracking email.

The clearer the tax explanation, the fewer after-sales disputes there will be.

Step 6: Build a Compliance File Library for Each SKU

In 2026, product compliance documents have become basic assets for cross-border sellers. Whether it is platform review, customs inspection, tax authority inquiry, or customer complaint, sellers may be required to provide product documents.

It is recommended to create a separate folder for each SKU, including at least:

Product name;

SKU number;

Supplier name and contact information;

Procurement contract or purchase record;

Purchase invoice;

Product images;

Product material description;

Product usage description;

HS Code;

Country of origin information;

Product test reports;

Compliance certificates;

Packaging label files;

Instructions and warning statements;

Batch number or production date;

Import declaration records;

After-sales, return, and complaint records.

If selling to the European Union, sellers should also prepare GPSR-related materials, including EU responsible person information, safety warnings, product identification information, recall contact information, and product traceability documents.

If the product is a children’s product, toy, electronic product, battery-powered product, personal care product, kitchen product, or skin-contact product, document requirements should be even stricter. Do not wait until the platform asks for additional materials before contacting the supplier.

Step 7: Standardize Orders, Invoices, and Financial Records

The core of tax compliance is complete records. Many sellers are not intentionally violating rules. Instead, their orders, receipts, refunds, platform fees, advertising costs, and logistics costs are not organized clearly, which makes their accounts difficult to explain later.

Sellers should organize at least the following data every month:

Sales by platform;

Shopify independent store sales;

Sales by country and region;

Payment platform receipt amounts;

Refund amounts;

Platform commissions;

Payment processing fees;

Advertising costs;

Procurement costs;

Logistics costs;

Tax costs;

Inventory changes;

Profit reports.

Pay special attention to the fact that platform backend sales, Stripe/PayPal receipt amounts, bank deposit amounts, ERP order amounts, and accounting report amounts may differ due to fees, refunds, exchange rates, and tax treatment methods.

These differences are not necessarily a problem, but they must be explainable.

Step 8: Regularly Check Whether Tax Registration Thresholds Have Been Triggered

Cross-border e-commerce tax obligations are not fixed. Just because you do not need to register today does not mean you will not need to register three months later. As orders grow, advertising expands, overseas warehouses are used, and platform sales increase, sellers may suddenly reach a tax threshold in a certain country or state.

It is recommended that sellers check key markets once a month:

Whether sales in each U.S. state are approaching economic nexus thresholds;

Whether EU distance sales exceed relevant OSS thresholds;

Whether IOSS is needed;

Whether UK sales involve VAT registration;

Whether Australian GST sales are approaching the threshold;

Whether Canada requires GST/HST or provincial tax registration;

Whether Singapore, Japan, and other markets have reached registration requirements;

Whether local tax obligations have arisen because of overseas warehouse inventory.

If a certain market is growing quickly, sellers should consult a professional tax advisor in advance instead of waiting until the platform freezes the account or the tax authority sends a notice.

Step 9: Write Compliance Responsibility into the Supply Chain Process

Many seller compliance risks come from suppliers. For example, suppliers may ship the wrong product, ship random colors, fail to provide test reports, use non-compliant labels, provide inaccurate declaration information, under-declare product value, or ship packaging without warning statements. All of these can affect the final seller.

Therefore, when choosing suppliers or dropshipping service providers, sellers should not only ask about price and shipping speed, but also confirm:

Whether they can provide formal invoices;

Whether they can provide product test reports;

Whether they can label products according to target market requirements;

Whether they support product and packaging customization;

Whether they can provide accurate declaration information;

Whether they can cooperate with returns, recalls, and after-sales service;

Whether they can provide stable SKUs and batch traceability;

Whether they can conduct quality inspection before shipment.

If sellers use a dropshipping service provider, the service provider should also participate in quality inspection, labeling, packaging, shipping, tracking number synchronization, and after-sales handling. This can reduce compliance risks caused by a chaotic supply chain.

Step 10: Build a Monthly Compliance Check Mechanism

Finally, sellers should turn tax and compliance into a fixed process rather than a temporary remedy.

It is recommended to conduct a basic monthly check:

Which countries saw significant sales growth this month?

Are any countries close to tax registration thresholds?

Has any platform requested additional identity or tax documents?

Have any products been complained about, delisted, or required to provide certificates?

Have any parcels experienced customs clearance issues?

Have any customers refused delivery because of customs duties?

Do any product labels, instructions, or warning statements need to be updated?

Have any suppliers changed materials, packaging, or production batches?

Do prices need to be adjusted to cover taxes and customs clearance costs?

Once this process becomes fixed, sellers can shift from passively responding to platforms and tax authorities to actively managing business risks.

9. The Most Common Compliance Mistakes Cross-Border Sellers Make in 2026

Mistake 1: Treating Platform Tax Collection as Full Compliance

Platform tax collection only solves part of the tax issue. It does not mean sellers no longer need bookkeeping, filing, invoice retention, or management of independent store orders.

Mistake 2: Under-Declaring Product Value

Under-declaring product value may reduce taxes and fees in the short term, but once discovered by customs, platforms, or tax authorities, it may lead to parcel detention, fines, customs clearance channel problems, and even damage to store and brand reputation.

Mistake 3: Not Distinguishing Between DDP and DAP

DDP means the seller bears import taxes, duties, and customs clearance responsibility. DAP usually means the buyer may need to pay taxes and fees at import. If an independent store says “taxes and shipping included” but actually asks customers to pay tax upon delivery, it is very likely to cause refusals and complaints.

Mistake 4: Trusting Suppliers Just Because They Say They Have Certificates

Certificates must correspond to the specific product, model, material, manufacturer, testing standard, and target market. A vague certificate screenshot cannot prove that your product can be sold in the United States, the European Union, the United Kingdom, and Australia.

Mistake 5: Long-Term Inconsistency in Accounts

Long-term inconsistency among platform sales, payment platform deposits, ERP orders, procurement costs, logistics costs, and bank statements is one of the main sources of future tax risk.

10. Compliance Suggestions for Cross-Border Sellers in 2026

First, calculate taxes and fees during the product selection stage. Do not wait until the product starts selling well before discovering that VAT, customs duties, logistics, and return costs have eaten up the profit.

Second, prioritize suppliers with complete documents. Low price should not be the only standard. Suppliers that can provide invoices, test reports, material descriptions, labeling support, and batch traceability are more suitable for long-term operations.

Third, independent store sellers should use tax tools and professional accountants. Shopify backend tax settings can only solve part of the problem. Real tax judgment still requires consideration of sales markets, shipping methods, inventory locations, and company structure.

Fourth, marketplace sellers should keep documents consistent. Business licenses, tax numbers, bank accounts, company addresses, VAT/GST information, warehouse addresses, and return addresses should be logically consistent as much as possible.

Fifth, when selling to the EU and UK markets, prepare VAT, IOSS, EORI, responsible person information, GPSR documents, product labels, and safety instructions in advance.

Sixth, when selling to the U.S. market, regularly check economic nexus in each state, especially after independent store orders grow. Do not rely only on platform tax collection.

Seventh, low-ticket products must be recalculated. After changes to low-value parcel policies in the United States and the European Union, taxes and customs clearance costs will have a more obvious impact on the profit of low-price small products.

Conclusion: Cross-Border E-Commerce Competition in 2026 Is Essentially a Competition of System Capability

Global e-commerce in 2026 has entered a more standardized, transparent, and data-driven stage. Sellers that can achieve long-term and stable growth in the future are not necessarily only those who are best at advertising or finding winning products, but those who can integrate product selection, supply chain, logistics, tax, product compliance, data privacy, and customer experience.

Tax and compliance may seem to increase operating costs, but they are also a protective moat for sellers. The earlier sellers establish a compliance system, the more they can reduce risks from platform reviews, customs detentions, tax recovery, and customer complaints.

For cross-border sellers, the most important thing is not to register tax numbers in every country all at once, but to establish a clear judgment process:

**Where are you selling? Where are the goods shipped from? Who is the importer? Who collects tax? Who handles customs clearance? Who files tax returns? Are product documents complete? Are the accounts consistent?**

Once this process is established, even if policies continue to change in the future, sellers can adjust quickly instead of waiting until platform review, customs issues, or tax notices appear before taking temporary action.

FAQ: Common Questions About Global E-Commerce Tax and Compliance in 2026

1. Do cross-border e-commerce sellers have to register for VAT or GST?

Not necessarily. Whether registration is required depends on the sales country, sales volume, shipping origin, inventory location, sales channel, whether the platform collects tax, and local tax thresholds. Sellers should assess each market separately rather than blindly registering in every country from the beginning.

2. If the platform already collects tax for me, do I still need bookkeeping?

Yes. Platform tax collection only means certain taxes are handled by the platform. It does not mean sellers do not need to keep order records, invoices, procurement records, logistics records, refund records, and income records. Corporate income tax, financial statements, and orders from other channels still need to be managed by the seller.

3. Does Shopify automatically handle global tax compliance for independent stores?

Not completely. Shopify can help set tax rates and display tax charges, but whether registration, filing, tax payment, IOSS use, or import tax handling is required still depends on the seller’s actual business situation.

4. Are small parcels under $800 still duty-free in the United States?

According to CBP information, imported goods valued at $800 or below from all countries are no longer eligible for de minimis duty-free treatment and must be subject to applicable duties, taxes, fees, and customs clearance requirements.

5. Do goods below €150 in the EU still need to consider customs duties?

Yes. The Council of the European Union confirmed that from July 1, 2026, small parcels entering the EU with a value below €150 will be subject to a temporary fixed customs duty of €3 per product category, planned to last until July 1, 2028.

6. What should dropshipping sellers pay the most attention to?

Dropshipping sellers should pay the most attention to three things: first, clearly define who is the importer and who bears taxes and duties; second, ensure that product labels, test reports, and compliance documents are complete; third, make sure customers know before placing an order whether extra customs duties or import taxes may occur.